From The Condo Report — your weekly Washington, D.C. condo and co-op briefing.

“I’m comparing two condos in D.C. — a one-bedroom in a 1970s building near Dupont Circle with an $810/month fee, and a similar unit in a new building in NoMa with a $385/month fee. The new building has more amenities. What is the older building’s fee actually paying for, and is the lower fee on the new build too good to be true?”

James: Excellent question, and one that should be asked far more often. D.C. condo fees vary widely — from under $400/month in some new construction to well over $1,500/month in full-service pre-war buildings — and the difference is rarely random. The fee is buying something specific. Once you know what to look for, that number tells you more about the building than the listing photos do.

Washington’s condo inventory spans roughly a hundred years of construction, from converted Victorians to 1960s mid-rises to brand-new towers on Half Street. A fee that seems high in one building can be a bargain in another. A fee that looks low can be the most expensive part of the purchase. Here’s how I read them.

A D.C. condo fee is buying specific things.

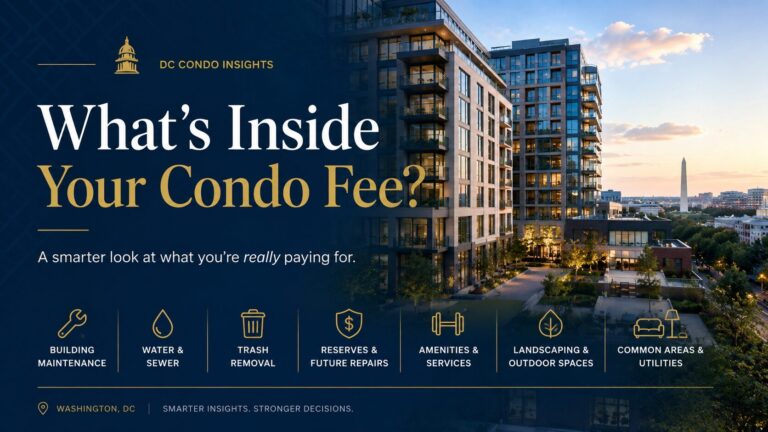

A condo fee isn’t a fixed cost like a mortgage payment. It’s an allocation. Every month, your dues are split across several line items, and the share of each varies enormously by building.

The big buckets are typically: operations and management (staff, cleaning, common-area utilities, landscaping, trash), master insurance, reserve contributions for major capital expenses, and amenities (pool, gym, concierge, parking attendants, package room staffing). Some buildings include water and gas in the fee; some don’t. Some still carry a master cable contract; most no longer do.

When you see two buildings with very different fees, almost all of the gap lives in the amenity and staffing lines. The cost of running a 20-unit brownstone with a part-time porter looks nothing like the cost of running a 200-unit full-service building with a 24-hour concierge, valet parking, and a rooftop pool.

Building size and age both matter — but not how you think.

Small buildings (under 30 units) tend to have higher per-unit fees because fixed costs — insurance, master policies, basic services — get spread across fewer owners. A roof replacement in a 12-unit building hits each owner harder than the same roof in an 80-unit building.

Older buildings carry more capital risk. Pre-war buildings along Connecticut Avenue or in Kalorama have beautiful bones, but those beautiful bones include 80-year-old plumbing risers, original elevator shafts, and masonry that needs repointing on a cycle. Well-run pre-war buildings price that risk into their fees and their reserve contributions. Poorly run ones don’t, and the bill arrives later as a special assessment.

Newer isn’t automatically cheaper to operate, either. Buildings with more glass, more mechanical systems, and more amenities have higher operating complexity even when the underlying physical plant is younger.

Amenities aren’t free, even when they feel like they are.

A rooftop pool sounds like a perk. It is, until you read the fee breakdown. A pool requires a permitted lifeguard service in season, mechanical maintenance year-round, and an annual deck and tile review. A 24-hour concierge desk requires roughly 4.2 full-time-equivalent employees once you factor in coverage, benefits, and overtime — call it $250,000 to $350,000 a year for the building to fund.

Spread across 100 units, that’s $200 to $300 per unit per month for the front desk alone, before anyone has turned a light on elsewhere. None of that is wasteful, but if you’ll never use the concierge or the pool, you should know you’re paying for them in every monthly statement.

The new-build fee is almost always the most misleading number on the listing.

This is the section to read twice if you’re shopping new construction.

Developers set initial monthly fees during the marketing phase of a building. The number isn’t determined by the building’s actual long-term operating cost. It’s set to a level that supports the unit pricing the developer wants. A $385/month fee makes a $700,000 condo feel affordable in the underwriting; an $800/month fee on the same unit doesn’t.

To get the fee that low, two levers usually get pulled. First, the initial reserve contribution is set at the minimum the lender and association documents will allow, often well below what a serious long-term funding plan would require. Second, the master insurance policy and the operating budget are priced on the building’s first year of stabilized occupancy — before claims history, before turnover, before the first round of capital work.

What follows, almost without exception, is a fee increase in years two through five. I’ve watched it happen in multiple D.C. new-construction buildings: an opening fee in the high $300s settles, two or three budget cycles in, into the $600s or $700s. The owners who bought on the strength of that opening fee feel ambushed. They shouldn’t — the math was always going to land here. The disclosure documents told them so, in dense paragraphs most buyers never read.

A lower fee today can be the more expensive number tomorrow.

The trade is simple in concept: you pay now through dues, or you pay later through assessments and steep fee escalations. Buildings that fund reserves properly look more expensive on the listing sheet and are usually the financially safer purchase. Buildings that suppress fees for marketing optics look like a deal until they aren’t.

This is the same diagnostic frame from last week’s piece on special assessments. The fee and the assessment are two sides of the same equation. A building that runs the fee low and gets surprised by a $15,000 capital project per unit didn’t save its owners money. It deferred the payment.

What to ask before you write the offer.

For any building, request:

- The most recent reserve study and the current percent-funded number. Healthy buildings target 70% or higher.

- The current operating budget and the prior two years for comparison. You want to see how the fee has moved.

- For new construction specifically: ask whether the developer is subsidizing operating costs in year one, and at what point that subsidy ends. The answer is sometimes in the disclosure documents, sometimes only in the developer’s pro forma.

- The age and remaining useful life of the major systems — roof, elevators, boilers, chillers, garage membrane. Those are the line items that drive future assessments.

The D.C. Department of Insurance, Securities and Banking publishes general consumer guidance on condominium associations, but the real diligence happens at the building level, in the documents.

So how should you compare those two units?

Lean toward the higher-fee Dupont building if the reserves are well-funded, the recent capital projects are documented, and the building’s run rate has been stable. The number isn’t pretty, but it tells you the truth.

Lean toward the NoMa new build if you’ve read the developer’s offering documents carefully, accept that the fee will rise meaningfully in years two through four, and can underwrite the unit at a fee that’s 50–80% higher than today’s. If that math still works for you, buy with eyes open.

The bottom line.

The single biggest mistake I see condo buyers make is treating the fee as a fixed input and the building’s reserves as someone else’s problem. The fee is the most informative line on the disclosure summary. Spend an hour with it before you write an offer, and you’ll know more about that building than most owners do after living there for a year.

If you’d like, send me the addresses of the two buildings you’re comparing and I’ll pull the current reserve study, percent-funded figure, and the last three years of fee history on each. That side-by-side usually answers the question faster than anything else.

— James Grant — Condo Report