From The Condo Report — your weekly Washington, D.C. condo and co-op briefing

May 27, 2026

Reader Question:

“My lender mentioned there’s some kind of Fannie Mae condo rule change coming this summer that could make financing harder. I’m getting ready to write an offer on a condo in Adams Morgan and now I’m wondering if this is something I actually need to worry about, or if it’s just one of those industry headlines that sounds scarier than it is?”

James:

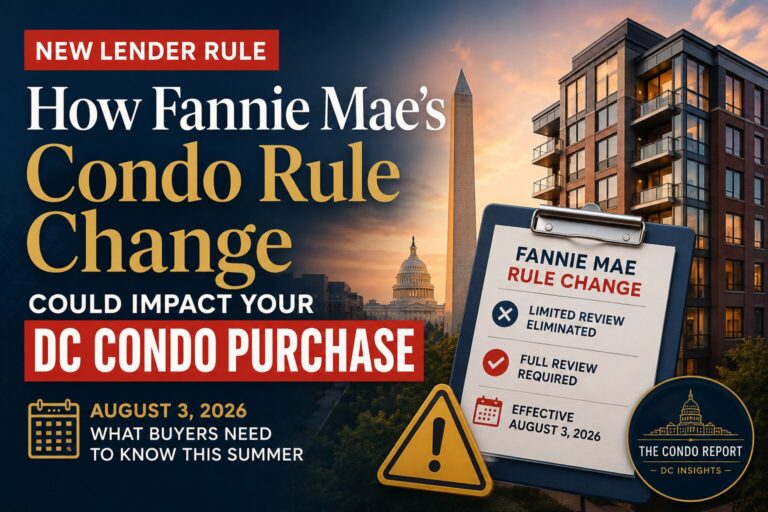

Not noise and if you’re thinking about DC condo financing in 2026, this one deserves your full attention. August 3, 2026 is the date Fannie Mae eliminates the Limited Review process for established condominium projects with more than ten units. If your loan application is dated on or after that date, your lender must run a Full Review on any condo building you’re trying to finance. The difference between the two matters more than most buyers realize, and the timeline is short.

Here’s what’s actually changing and what it means for your offer in the DMV.

Limited Review vs. Full Review: what you were getting before.

Until August 3, most lenders have been able to approve a condo purchase using Fannie Mae’s Limited Review process. Limited Review was designed as a streamlined pathway: the lender checks a few key items — the owner-occupancy ratio, whether the HOA is involved in active litigation, and whether the master insurance is in order — but doesn’t dig deeply into the reserve study, underlying financial health, or the association’s capital plan.

It was fast. It worked for the majority of well-run buildings. And it kept DC condo transactions moving without requiring a full financial disclosure from every association. After August 3, Fannie Mae eliminates it entirely for established projects with more than ten units.

What Full Review actually looks at.

Full Review is a more thorough underwrite of the building — not just your unit and your credit. Your lender will require the condominium questionnaire completed by the building’s management company, covering: reserve funding percentage, owner-occupancy ratio (minimum 50% for most loan types), any special assessments active or pending, current litigation involving the HOA, master insurance coverage limits, and the percentage of units delinquent on dues.

For buildings that are professionally managed, financially stable, and reserve-funded at or above 10%, Full Review is a procedural hurdle, not a barrier. For buildings with low reserve funding, deferred maintenance items, or management companies that are slow to return lender questionnaires, Full Review is where deals die.

How condo financing changes on August 3.

The practical issue isn’t that Full Review is impossible — it’s that Full Review surfaces building problems that Limited Review quietly ignored. A building that was technically financeable under Limited Review in March may not clear Full Review in September if its reserves are thin, if it has a deferred capital project, or if its management company takes three weeks to return a questionnaire.

The second pressure point is the 2027 reserve increase. Starting January 4, 2027, Fannie Mae raises the minimum reserve allocation from 10% to 15% of annual operating budget. Buildings in the 10%–14% range are in a squeeze: they’re funding at the current minimum but will need to raise dues or run special assessments to hit the new floor. For more on how DC condo financing has been shifting, see the DMV condo rate math breakdown from earlier this year.

Which buildings in the DMV are at risk.

The buildings most exposed are in the 10%–15% reserve funding range. In Washington, D.C., those tend to be older pre-war cooperatives and mid-century condominiums — many managed by boards that haven’t updated their reserve study in several years. The Connecticut Avenue corridor and Foggy Bottom both have buildings worth checking. If you’re shopping Capitol Hill’s older condo stock, ask about the reserve study before you schedule a second tour, not after.

Buildings where the management company is slow or unresponsive to lender questionnaires are a separate risk category. A building with adequate reserves that takes four weeks to respond to a Full Review questionnaire can still blow your closing. Ask your agent or lender if they’ve worked with this building’s management company before — that relationship matters now more than it did under Limited Review.

Insider Secret: The Boutique Building Sweet Spot

One smart condo strategy right now is to look at smaller boutique buildings.

The DMV has thousands of them — especially 4-to-10 unit conversions in DC neighborhoods like Columbia Heights, Dupont, Shaw, Adams Morgan, and Capitol Hill, plus smaller garden-style communities in Arlington and Silver Spring.

Why does this matter? Under Fannie Mae’s updated condo rules, projects with 10 or fewer units may qualify for a Waiver of Project Review, meaning they can potentially avoid the heavier full condo review process that larger buildings now face. For 5-to-10 unit buildings, the project generally cannot be part of a master association or larger development.

Translation: a well-run boutique condo building may offer a cleaner financing path, less lender friction, and a faster path to the closing table.

This does not mean every small building is automatically approved — we still need to check the details — but it does create a very real “sweet spot” for buyers who want to avoid getting caught in condo review quicksand.

Three moves that protect you before you offer.

- Ask the condo board today if they are preparing their 2027 budget to meet the 15% threshold. If they aren’t, your listings in that building will soon face a massively restricted buyer pool.

- Ask your lender to run a preliminary building review before you’re under contract. Several DC-area lenders will do a quick pre-offer review to flag obvious disqualifying factors. It doesn’t take long and it’s free — and the ones who offer it unprompted are the ones worth working with.

- Look closely at the “Reserve Allocation” line item in the budget during your 3-to-5 day condo document review period. If it sits exactly at 10%, warn your buyer that their monthly condo fees are highly likely to spike next year as the board scrambles to hit 15%.

For context on how DC condo buying compares across the region, the DC vs. Virginia vs. Maryland breakdown is worth a read if geography is still open.

So which is the right move right now?

Lean toward moving sooner if you’re ready. DC condo inventory is the highest it’s been in years, prices have softened roughly 9% from Q1 2025, and rates are sitting near 6%, down almost a full point from the 7% plus environment of the past two years. Add a rule change that creates uncertainty after August 3 and the calculus gets clearer: the next six to eight weeks may be the most buyer-favorable window of the year.

Lean toward waiting if you need the time — but go in eyes open. Know your building’s reserve status before you offer. Confirm your lender is building toward a Full Review timeline. The good news: a building that passes Full Review is a better building than one that passed only under Limited Review.

The bottom line.

The single biggest mistake I’m seeing buyers make right now is assuming that lender approval means building approval. Your credit is one underwrite. The building is another. After August 3, those two underwrites happen in parallel and the building one gets harder. The fix is straightforward: get the building questionnaire and reserve study before you fall in love with a unit, not after you’re under contract.

Send me the addresses of any buildings you’re considering and I’ll pull what I can on reserve status, owner-occupancy, and recent comp history. Fannie Mae’s full announcement is at singlefamily.fanniemae.com (LL-2026-03) if you want the primary source.

— James Grant — Condo Report